{kind=link}

Rapaport to be blamed for Industry Failure, not De Beers!

For over 35 years, the Rapaport Group has been publishing a weekly price list for colorless diamonds. What started as a hobby by its founder became the industry wide standard. You can find the first ever Rapaport list still hanging on the wall at the head office in Ramat Gan, Israel to remind us of the beginning of the end. Since those days, the Rapaport Group has also launched a diamond sales platform called Rapnet to allow for worldwide online diamond trading for industry participants, among the myriad of other services that they offer.

The turning point for the diamond industry market control was back in 2014 when the diamond market was faced with greater uncertainties. Martin Rapaport did what he did on any given week, reviewing and updating his price list according to his usual calculations. Only this time, it featured a huge drop in prices. It affected all those that feed him (via the membership fees that they pay to the Rapaport Group), causing many raised eyebrows at the sudden and significant change. There is also a significant conflict of interest that exists because Rapaport trades his own inventory despite the fact that he establishes prices on the Rap List. That can be a major cause for concern in his overall judgement in dropping the prices.

Over 1 million stones are listed for trade on Rapnet with over $8 billion in value, the online trading network for the industry’s buyers and sellers. When Rapaport revises this list in one way or another, the whole entire industry is greatly affected. This is because diamond dealers sell most goods (including on Rapnet) at a discount to the listed prices of the Rap List ,or on rare occasion at a premium price to the list. When the list is revised upwards, valuation of inventory goes up and when the price list is revised downwards, valuation moves accordingly. In short, the Rapaport List can take businesses up or down in one fell swoop. The Rapaport list directly affects the diamond prices of the diamonds on Rapnet (which you will recall is greater than 1 million in number and $8 billion in value).

Not everyone in the world was willing to sit back and let this continue. One morning during March 2015, the majority of dealers in the world, predominantly those that are located in India, decided to put the brakes on Rapaport and counter attack. They all listed their inventory on Rapnet at the Rapaport List prices (not below them). This in turn completely changed the game. No longer were the dealers allowing Rapaport’s judgement calls to dictate the game.

If you pay attention to diamond industry trends, you may have noticed that in the last few months, the Rapaport Index report has been a representation of “the average price for the top 25 diamond qualities (D-H, IF-VS2). it is based on the 10 best priced diamonds for each quality”. Is that even a proper representation of the industry? Can we trust this data? Why do we trust this data?

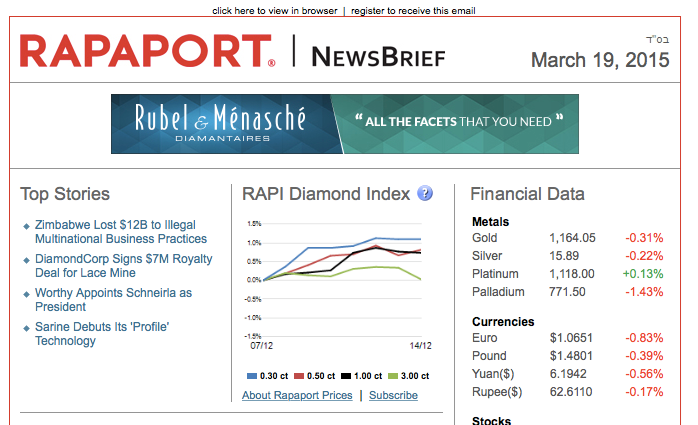

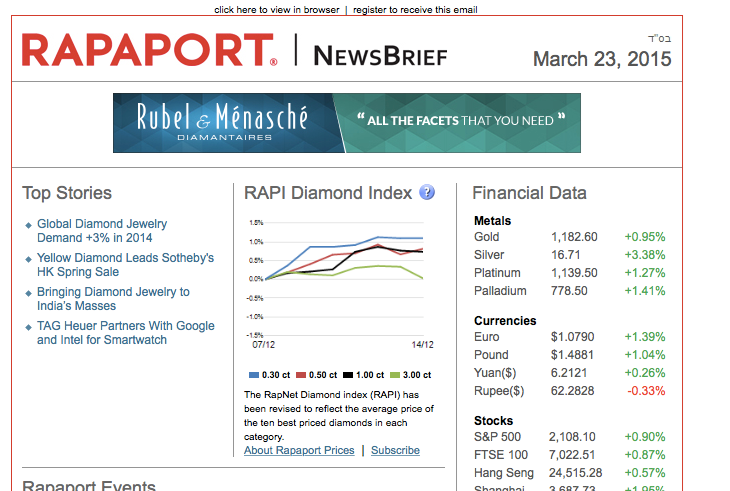

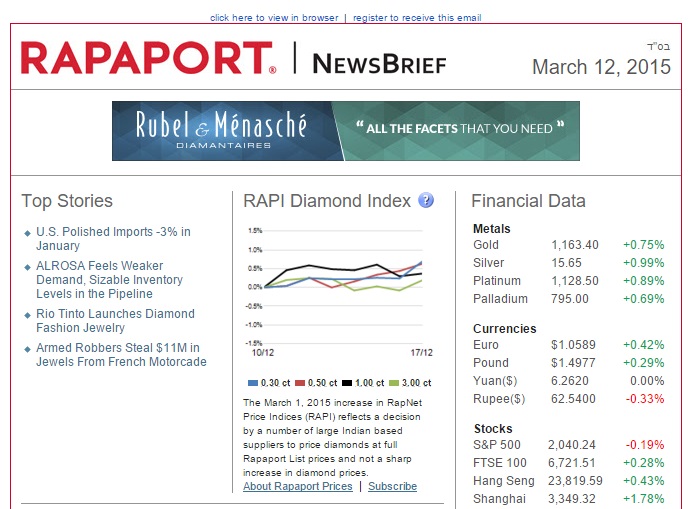

A view of the March 2015 RAPI Diamond Index prior to changes

A view of the March 2015 RAPI Diamond Index after the changes

A view of the March 2015 RAPI Diamond Index with commentaries

Why should De Beers fall to the pressure of Rapaport?

As a for profit organization, De Beers, like any other company out there in the world, has the right to charge or ask whatever price it wants for its products (as does any other diamond producer for that matter). In any industry, be it cars, food, clothing, or housing, the producer or manufacturer may ask his clients or any other potential client for any price for their goods. We are all capitalists in one way or another. If a polisher or manufacturer does not wish to accept the price that they are being quoted, they have the right to walk away from a deal. If enough manufacturers walk away, De Beers, and any other producer of rough diamonds, will realize that the prices are too high and will naturally reduce them to a level where the buyer will feel that they can buy product, transform it, and sell it for a profit. It is the basic economic law of supply and demand.

Martin Rapaport, in his monthly Rapaport newsletter, recently released an article blaming De Beers for artificially, prohibitively high rough diamond prices. As a supposed champion of the ‘everyman’ polishers and manufacturers, he elaborated over 6 pages how De Beers is essentially at fault for the current situation in the diamond industry. His claim is that the high prices for rough diamonds are causing all of the diamond trade to fall like dominoes as small- to medium- sized diamond manufacturers cannot meet the prices of the rough diamonds in order to buy, cut, polish and resell for a profit. He states that the profits are nonexistent because the diamond miners are greedily charging exorbitant prices for rough diamonds, forcing the polishers to borrow enormous loans from banks to pay for the goods. The banks were happily lending the money to the diamond industry and willing to only collect the interest payments for the loans because they had no problem with the money being funneled essentially directly to the mining companies, until the debt has now piled so high that even the banks are slowly pulling away from this scheme. Coupled with the fact that consumer demand for diamonds has remained relatively low due to the worldwide economic situation, it is as though the polishers and dealers are suffering from three fronts – De Beers’ prohibitively high prices, low consumer demand, and no more bank loans. By Martin Rapaport placing the blame squarely on De Beer’s shoulders, he is calling on them to take the hit and lower rough diamond prices ‘in order to save the industry in the long term’. This would allow the polishers a higher profit margin in the sales of their goods and allow them to recover.

Martin’s claim differs from the premise above in that he claims that the blame lies squarely in De Beer’s hands, while he does not acknowledge what was established above that if enough cutters, polishers, and manufacturers simply rejected the mining companies’ prices, that very factor would cause the price of rough diamonds to go down regardless (with De Beers and the other diamond mining companies taking the same hit). Martin calls on De Beers to do this and does not recognize the basic laws of economics that if only the same companies that rejected the RapNet tradition of listing below list price would use that same power and reject the prices of De Beers they could make another huge change for the second time in less than 2 years. Is there denial here about their power to affect change in the diamond industry? Rapaport makes a big claim in the article by saying that De Beers may have a master plan to eliminate the diamond trade entirely and eventually sell directly to the consumer, seemingly completely minimizing the diamond trade’s power and influence. He also entirely glossed over another 2 solutions to alleviate the situation – the retailers could charge less for the finished goods, causing consumer demand to rise and subsequently all demand to rise up the product manufacturing chain (higher demands for polished goods, higher demands for rough demands), which would translate into an improved situation for everyone – not just the polishers. Another solution is elaborated on below – stop putting out a price list and there will be no prices that the polished diamonds are held to, thus allowing for free market forces to determine the prices paid for goods and better profit margins to be earned.

So what came first? The chicken or the egg?

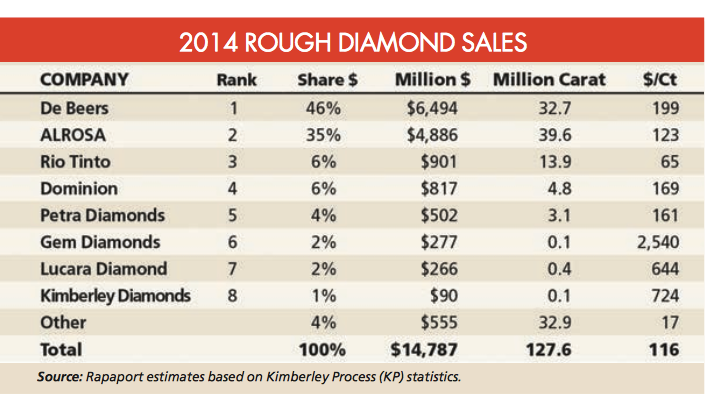

We all know that De Beers at one time was controlling not only the supply of diamonds but also their prices. We also know that since the late 1990’s De Beers lost that privilege, yet most polishers still believe it to be true. According to the Rapaport report, De Beers now controls about 46% of dollar sales but only 32.7% of volume, meaning that it no longer holds control. In fact, ALROSA produces more diamonds than De Beers does. According to Rapaport’s own report, De Beers does not have the power and control over the industry that the above mentioned Rapaport article is claiming that it has! This is interestingly contradictory. According to the table below, which is also part of the report that was written, there are 8 major companies controlling the market, and just 4% of the market is controlled by all the other smaller players. As you can see in the table, De Beers makes the largest amount of dollar sales but does not produce the most diamonds.

Mr. Rapaport, I have a question about this table: how come these 8 combined companies control 102%? Not to mention the last 4%, which totals 106%…. My calculator says that De Beers should be at 44%, Alrosa at 33%, and so on – according to the $ figures from your own table.

Diamond mining companies’ market shares

Polishers should make their own choices

For a short explanation of how buying from De Beers works – 90% of De Beers’ rough diamonds are sold by value to customers known as Sightholders, at events called Sights. This practice has existed now for a long time.

Polishers should have walked away from sights long ago. I think that polishers did not for a simple but innocent reason, believing that De Beers would simply replace them and they would just lose their supply. They did not believe that their walking away could have the effect that they desired. And if they had walked away from the sight system? If they were not making money anyway, why would they continue buying something at a dollar just to sell it at $0.90? What kind of business owner does that? Every business knows that they make money on 1 product, while losing on another, and yet at the end of the year they make money on their overall sales. However, it seems that polishers were losing money at the end of the year given both of those aspects of business. If I was a polisher, I would have shut down and moved on to another business!

Polishers were also falling to the pressure of traders not willing to buy the goods above a certain price, and therefore worked on very lean margins of no more than 2-3% (according to a Bain & Co. Report) because of the high prices of the rough diamonds and low prices of the polished diamonds. Every business owner makes his own decision on how to run his business, and if their price structure is not accepted by the client, it is up to him to decide to whether to reduce the price accordingly or to walk away from the deal (in this case, walking away from the rough diamond prices in order to ultimately save their margins). It certainly does not make sense to end the year at a loss. Polishers are viewing themselves as still beholden to the sightholder system despite the fact that the Rapaport report clearly shows that De Beers is no longer the main mine in town. Perhaps it is because they are so used to the system, afraid to lose the prestige of being a sightholder, or are afraid to lose what they think would be their only pipeline of goods. Regardless of the psychological justifications – eliminate the sights and the money that the polishers require to buy at sights, and the polishers would be rescuing their own operations.

Should Dealers & Traders Depend on Rapaport?

Walk into every dealer of colorless diamonds at any office of a diamond exchange and right in the middle of their desk you will find the famous red Rapaport price list. It seems that their business revolves around that red paper, whether they like it or not (which, by the way, just humorously gave me the mental visual association with the Chinese communist regime controlling their citizens). Are all the dealers just mere managers of their own businesses, and Rapaport the true owner? I recall listening to dealers’ troubles last year, when times were already starting to be tough, and yet Rapaport continued to reduce the price list. People were losing money just holding inventory!

The Rapaport famous red Price List Courtsey of rapaport

No other industry has a price list controlled by one entity like the diamond industry. Where is the natural freedom to trade at the value both parties agree on (the beating heart of capitalism)? There is a product, and there is a buyer and a seller. Both see value in the product. For how much should the seller sell it? At what price should the buyer buy it? At the exact price that both feel comfortable buying and selling, knowing each can make money in the transaction. Profit margins are therefore naturally determined. Microeconomics 101. Its that simple and eliminating the Rapport list that controls this margin would absolutely dig out the polishers from their woes.

Retail Shops May Also be at Fault

What about shops and stores? What is their role in the value chain? We all know that they account for the largest and fattest profits in this value chain. Maybe they are at fault for reduced demand by consumers? If consumers have less spending money now than previous years, shouldn’t the retailers adjust prices accordingly? Just look at the table below, presented year after year by Bain & Co. and the AWDC. It is clear that retailers account for the largest profits. Yes, we know that they have their own expenses to cover and many other components come into play, but still, there is some blame here for them to absorb. Like I stated above, lowered prices would lead to greater demand and subsequently greater demand along all of the steps of the value chain, improving the market for all! (This is actually the solution that benefits the most market players).

What Role Do E-Tailers Play in the Value Chain?

One day in the not so far past, somebody decided that they will open a website, and sell diamonds and jewelry over the internet. What a revolution! Cut the fixed cost of stores in malls, cut staff costs, stay open 24/7 and pass on some of those savings onto consumers. Yet even 20 years later, online jewelry sales still account for far less than 20% of all sales. There is still the magical moment of walking into a store and physically attaching oneself to the dream, to love. However, the fact that consumers are looking for outlets other than the retailers in order to buy product at a price that they are more willing to pay is a clear demonstration of the fact that if retailers lowered prices, they would absolutely increase aggregate demand and the solution above would be kick started into full gear.

Revolution

The first revolution in this industry took place on March 1, 2015, when the majority of large Indian dealers and polishers decided that they had enough with Rapaport “controlling” their destiny and decided to put an end to it! What did they do? As I mentioned above, they priced all their inventory on Rapnet at the Rapaport suggested price list’s list prices. This completely distorted information for Rapaport and his data bank of information on which he relies. Look at the various index tables from back in March 2015 in the image above. Look at the text below the tables (really, the lack thereof). Nowadays, it reads “the Rapnet Diamond Index (RAPI) is the average price for the top 25 diamond qualities (D-H, IF-VS2). It is based on the 10 best priced diamonds for each quality”. Is this a true index? Is this a true representation of the industry? What about the other colors and clarities? Do they not play an important role to understand true diamond value and the industry’s status? We all know that current major demand by less developed countries or countries who are building this industry currently demand lower quality goods in the SI clarities, and lower than H color. Why not have sub-indices in order to comprehensively represent the market? Is the RAPI as it currently stands a proper representation of data? All of these questions essentially raise the point that given all of the trust that the industry puts into Rapaport’s hands, maybe they should be more skeptical instead. Making decisions and deductions on incomplete data may have been the trend in the past but certainly does not need to continue. Maybe after taking a closer look, dealers will realize that they should ditch the incomplete Rap List altogether, with the obvious benefit that the data is incomplete and wasn’t properly contributing, but also that selling according to agreements between buyers and sellers would allow for significantly better profit margins for both parties as market forces would finally properly be at play.

The current representation of the RAPI

The Industry is Undergoing Fundamental Structural Change Anyway

“The industry is undergoing fundamental structural change” – this is 1 of probably only a handful of comments that Martin Rapaport made in his report with which I agree. Every industry goes through inevitable changes and evolution as it moves forward due to technology or any other reason to which it may be subjected. The diamond industry, like most industries, once resembled a pyramid. On top we had the miners, who sold to polishers, who sold to traders and suppliers, who sold to distributors, then on to retailers, and finally was sold to consumers, adding a desired profit margin at every step, exactly like many other industries. Now, the pyramid style business has transformed and will continue to transform until it will reach a balanced and harmonious form of…a circle. What is this circle? There are just 2 players; a buyer and a seller. Who really dictates prices? Who at the end of the day really has the power? Consumers and their money. Money is king.

Take the 1,111 carat rough white diamond that was discovered by Lucara Diamond Corporation, announced on November 19 of this year. The company’s CEO commented not long ago that he will entertain a $60 million offer on the rough. That is a very nice number, but, if no buyer values the rough at that price, well then Mr. CEO, you will not get your desired price. I am not suggesting that the rough is not worth that much as I have not yet seen it, and it just might be a bargain at this price. An expert polisher (one of many) will inspect and will calculate the best yield and then a humble calculator will take over and will decide the numerical value of the diamond. We have seen many large rough diamonds sell well above the $54,000 per carat that Lucara is looking for, but $60 million is still a large sum for any buyer to fork up. However, Lucara will only get as much as their top buyer is willing to pay for the diamond, and not more than that. This is entirely the concept of power in the hands of the consumer embodied.

The 1,111 carat rough diamond

Going back to my point – E-tailers came into the game and carved a piece out of the retailers’ business. Consumers desire to acquire diamonds for less money, and they are doing it in the same way that they have done in many other industries, by cutting out the most middle men possible from the value chain, turning that pyramid into a circle. Aren’t De Beers and Argyle doing just that, but reversed? De Beers the mining company started De Beers Diamonds and opened shops to sell directly to consumers (as I mentioned above, Martin Rapaport asked De Beers if they have the intentions of cutting dealers away out of the value chain…was Rapaport not aware that De Beers already has their own retail outlets? If so, why is he asking? The answer would be obvious. And if he did not know, now he does!) Argyle came to an agreement with jewelry company Chow Tai Fook and launched a jewelry line, cutting out many suppliers and wholesalers from the value chain. And really, what is wrong with that? Producers certainly need to worry about their own survival. These two companies are also definitely embracing the circle!

Producers also have to answer to their shareholders at the end of the day. If De Beers reduces their price by the 30-50% that Rapaport is calling for, then how will shareholders react? What will happen to the share price of Anglo-American? Companies are under constant pressure by shareholders for profits now more than ever. Rapaport can’t really expect that De beers will absorb all of the hit here, especially since so many other solutions exist in the market that will accomplish the same goal for the polishers!

Future Profits

I challenge Rapaport to do the easiest solution (effort-wise for himself) and to truly be the champion of the polishers that he is trying to be – stop publishing a price list! Yes that is exactly what I am saying. Will he? I am challenging him with the same manner as he is doing to De Beers! What do you think will happen if he does? And I am not referring to the ramifications to his organization the Rapaport Group that employs many people and has its own expenses to pay (maybe he can just continue trading his own inventory?). I am referring to the industry. Traders and wholesalers will still survive. Those that know the value of goods will remain, those that do not, will close up shop. There will be free trade, and polishers will start making money again. Sounds like economic force paradise.

There will be major M&A (mergers and acquisitions), as well as major consolidations. Some people in the value chain will undoubtedly have to go. Producers will most likely start buying up polishers, maybe some polishers will join forces with big dealers, and maybe some dealers will join forces with retailers. All of this will create value, by actually reducing costs across the board, just like any other major M&A announced daily in the news. New companies and entities will also arise as profits return to the table and new players will be thirsty to gain some for themselves, all to the benefit of consumers who will have a larger selection of goods available and at better prices than before.

Maybe companies from across the value chain should look at the king of diamonds, Mr. Lawrence Graff, and Mr. Lev Leviev. They are vertically integrated and carved themselves a piece of everything. They each own portions or even full diamond mines, they polish, and they set into jewelry and sell to consumers. Of course, they both deal with the highest ends of the affluent consumers, but nevertheless they should be the examples of how business is done. They are both extraordinarily successful and completely flout the pyramid system.

Conclusion

Rapaport should take responsibility and admit that his actions are partially responsible for the mess that this industry is in. Various players from the industry should reconsider how they manage and operate their businesses. All the entities should look into consolidating their businesses with complimentary ones. If the industry as a whole will take a step back, put their egos aside for a second, and work as a team, they will be able to push the industry as a whole forward. It will be a win-win for everybody, especially the consumer, who in the meantime is losing confidence in the industry, and walks to the next door shop and acquires an alternative product instead, a surefire death sentence to any industry.

I invite everybody to get on the bandwagon and work together for the sake of everybody. But remember one thing, diamonds are forever! The question is who will remain forever with them….

Wondering about anything or even disagree? Let me know in the comments below!

Related Posts

- Is Diamond Investing Well Worth The Risks Involved?

- Argyle Tender Is A Financial Vaccine, Becoming The Bitcoin Of Pink Diamonds As Covid-19 Continues On Its Global Rampage

- Magnificent Jewels Auctions In New York Successfully Seals 2020 Despite Virus Challenge

- Sotheby’s Magnificent Jewels In New York Is Set To Be The Best This Year For Fancy Color Diamonds

- Christie’s Magnificent Jewels Not So Magnificent This December

ЗА ПРОВАЛЫ В ОТРАСЛИ СЛЕДУЕТ ВИНИТЬ НЕ DE BEERS, А РАПАПОРТА!

В течение более чем 35 лет, Rapaport Group публикует еженедельный прайс-лист на бесцветные бриллианты. То, что началось, как хобби ее основателя, стало широко используемым стандартом индустрии. Вы можете найти самый первый прайс-лист Rapaport висящим на стене в головном офисе в Рамат-Гане, Израиль, чтобы напомнить нам о начале конца. С того времени Rapaport Group также запустила платформу для продажи алмазов под названием RapNet для обеспечения во всем мире онлайн торговли бриллиантами для участников отрасли, среди множества других услуг, которые они предлагают.

Переломным для контроля рынка алмазной промышленности явился 2014 год, когда алмазный рынок столкнулся с большими неопределенностями. Мартин Рапапорт сделал то, что он делал на любой данной неделе, пересматривая и обновляя свой прайс-лист в соответствии с его обычными вычислениями. Только на этот раз, он показал значительное падение цен. Это отразилось всех тех, кто его содержит (с помощью членских взносов, которые они платят в Rapaport Group), в результате чего у многих возникло недоумение от внезапного и значительного изменения. Существует также значительный конфликт интересов, поскольку Рапапорт продает свои собственные алмазы, несмотря на то, что он устанавливает цены в своем прайс-листе. Это могло быть основной причиной для беспокойства в его общей оценке снижения цен.

Более 1 миллиона камней стоимость свыше 8 млрд. долларов перечислены для торговли на RapNet, онлайн торговой сети для покупателей и продавцов отрасли. Когда Рапапорт пересматривает этот список в ту или инуюсторону, то от это в значительной степени зависит вся индустрия в целом. Дело в том, что алмазные дилеры продают большинство товаров (в том числе и на RapNet) с дисконтом к перечисленным ценам прайс-листа Рапапорта или в редких случаях по цене, превышающей указанную в прайс-листе. Когда лист будет пересмотрен вверх, оценка запасов идет вверх и когда лист пересмотрен в сторону понижения, оценка движется соответственно. Короче говоря, список Рапапорт может одним движением повысить или понизить оценку бизнеса. Лист Рапапорта непосредственно влияет на цены алмазов на RapNet (которые как Вы помните, составляют более 1 млн в количестве и в стоимости более $ 8 млрд).

Не все в мире были готовы сидеть, сложа руки, и позволить этому продолжаться. Однажды утром в марте 2015 года, большинство дилеров в мире, преимущественно тех, которые находятся в Индии, решили остановить Рапапорта и контратаковали. Все они указали свои запасы на RapNet по ценам листа Рапапорта, а не ниже них. Это, в свою очередь, полностью изменило игру. Дилеры более не позволили суждению Рапапорта диктовать правила игры.

Если вы обратите внимание на тенденции алмазной промышленности, то вы, возможно, заметите, что в последние несколько месяцев, в докладе Индекс Рапапорт была представлена “средняя цена за топ-25 параметров бриллиантов (D-Н, IF-VS2). Она основана на 10 самых дорогих бриллиантов для каждого качества “. Правильное ли это представление индустрии? Можем ли мы доверять этой информации? Почему мы доверяем этим данным?

RAPI Diamond Index от марта 2015 до изменений

RAPI Diamond Index от марта 2015 после изменений

RAPI Diamond Index от марта 2015 с комментариями

Почему De Beers должна уступать давлению Рапапорта?

Как и любая коммерческая организация в мире, De Beers, имеет право взимать или запрашивать ту цену на свою продукцию, которую она хочет (как поступает и любой другой производитель алмазов в этом случае). В любой отрасли, будь то автомобили, продукты питания, одежда, или жилье производитель может запрашивать у своих покупателей или любых потенциальных клиентов любую цену на свои товары. Мы все капиталисты в той или иной степени. Если огранщик или производитель не желает принять цену, которую с них запрашивают, они имеют право уйти от сделки. Если достаточное количество покупателей уйдет, то De Beers и любые другие производители необработанных алмазов поймут, что цены слишком высоки и, естественно, снизят их до уровня, когда покупатель будет чувствовать, что он может купить товар, обработать его и продать для получения прибыли. Это основной экономический закон спроса и предложения.

Мартин Рапапорт, в его ежемесячном информационном бюллетене Rapaport, недавно выпустил статью, обвинив De Beers в искусственном создании непомерно высоких цен на алмазное сырье. Предполагаемый защитник прав огранщиков и производителей, он посвятил более 6 страниц описанию того, как De Beers по существу является виновником ситуации, сложившейся, в алмазной промышленности. Он заявляет, что в результате высоких цен на алмазное сырье торговля алмазами развалится как домино, так как малые и средние производители алмазов не смогут выдержать цены на необработанные алмазы для того, чтобы купить, огранить и перепродать их с прибылью. Он утверждает, что прибыли не существуют, потому что жадные алмазодобывающие компании назначают непомерно высокие цены на алмазное сырье, заставляя огранщиков брать огромные кредиты в банках для оплаты товаров. Банки радостно кредитуют алмазную отрасль и готовы собирать только процентные платежи по кредитам, потому что у них не было проблем с тем, что деньги направляются по существу непосредственно добывающим компаниям, пока долг не достиг таких высот, что даже банки медленно отстраняются от этой схемы.

В сочетании с тем, что потребительский спрос на бриллианты оставался относительно низким из-за мирового экономического положения, получается, что огранщики и дилеры принимают удар на трех фронтах – непомерно высоких цен De Beers, низкого потребительского спроса, и отсутствие банковских кредитов. Мартин Рапапорт возлагая вину на плечи De Beers, призывает их принять удар и снизить цены на алмазное сырье «для того, чтобы спасти индустрию в долгосрочной перспективе». Это позволит огранщикам увеличить прибыль при продаже своих товаров и позволить им восстановиться.

Претензии Мартина, в которых он утверждает, что вина полностью лежит в руках De Beers, отличаются от того, что было установлено выше, что если достаточное огранщиков и производителей просто отклонило бы цены добывающих компаний, то этот фактор сам по себе заставил бы цену алмазов опуститься ниже (а De Beers и другие алмазодобывающие компании, приняли бы аналогичный удар).

Мартин призывает De Beers сделать это и не признает основные законы экономики, что, если только те же компании, которые отвергли на RapNet традиции листинга ниже прейскурантной цены использовали ту же силу и отвергли цены De Beers, они могли бы сделать еще одно огромное изменение во второй раз менее чем за 2 года. В их ли силах повлиять на изменения в алмазной промышленности? Рапапорт делает утверждение в статье, говоря, что у De Beers может иметься генеральный план полностью устранить торговлю алмазами и, в конечном итоге, продавать бриллианты непосредственно потребителю, совершенно сведя на нет влияние торговцев бриллиантами. Он также полностью умалчивает о еще 2 решениях, которые могут облегчить ситуацию – розничные торговцы могут назначать меньшие цены на готовую продукцию, в результате чего потребительский спрос будет расти и в дальнейшем это повлияет на подъем всей цепочки (более высокий спрос на бриллианты, более высокий спрос на неограненные алмазы), что отразится на улучшению ситуации для каждого – не только для огранщиков. Другое решение – остановить выпуск прайс-листа и убрать цены, которых придерживаются продавцы ограненных алмазов. Это позволит свободным рыночным силам определить цены, уплаченные за товары и увеличить получаемую прибыль.

Так что было первым – курица или яйцо?

Мы все знаем, что De Beers в свое время контролировала не только поставку алмазов, но и их цены. Мы также знаем, что с конца 1990-х годов De Beers потеряла эту привилегию, но большинство огранщиков все же считают, что это правда. Согласно докладу Rapaport, компания De Beers теперь контролирует около 46% продаж в долларах, но только 32,7% объема, это означает, что она больше не имеет полного контроля. На самом деле, АЛРОСА производит больше алмазов, чем De Beers. По собственным словам Рапапорта, De Beers не имеет власти и контроля над отраслью, но в упомянутой выше статье Рапапорт утверждает, что она имеет! Это интересное противоречие. Согласно таблице, которая также является частью доклада, существует 8 крупных компаний, контролирующих рынок, и только 4% рынка контролируется всеми другими более мелкими игроками. Как вы можете видеть в таблице, De Beers делает большинство объема продаж в долларах, но не производит большинство алмазов.

Г-н Раппапорт, у меня есть вопрос по этой таблице: как же эти 8 компании совместно контролируют 102%? Не говоря уже о последних 4%, что составляет 106% …. Мой калькулятор говорит, что De Beers должен быть на уровне 44%, АЛРОСА в 33%, и так далее – в соответствии с $ цифрами Вашей собственной таблицы.

Рыночная доля алмазодобывающих компаний

Огранщики должны сделать свой выбор

Для информации, как работает покупка у De Beers – 90% необработанных алмазов De Beers продаются клиентам, известным как сайтхолдеры, на мероприятиях, называемых Sights. Эта практика существует уже в течение длительного времени.

Огранщики должны были покинуть Sights уже давно. Я думаю, что они не сделали этого по одной простой причине, полагая, что De Beers просто заменит их, и они просто потеряют товар. Они не верят, что их уход может иметь желаемый эффект. А если бы они ушли от системы Sights? Если они не получали прибыль в любом случае, почему они продолжают покупать что-то на доллар и просто продавать это по $ 0,90? Какой бизнесмен так поступает? Каждый бизнес знает, что они делают деньги на 1 товаре, в то время как теряют на другом, и все же в конце года получают прибыль с общего объема продаж. Тем не менее, кажется, что огранщики теряли деньги в конце года по обоим аспектам бизнеса. Если бы я был огранщик, я бы закрылся и перешел в другой бизнес!

Огранщики также поддаются на давление трейдеров, не желающих покупать товар выше определенной цене, и, следовательно, работают за очень скудные прибыли – не более чем 2-3% (согласно докладу Bain & Co.) из-за высоких цен на необработанные алмазы и низких цен на бриллианты. Каждый владелец бизнеса принимает свое собственное решение о том, как вести свой бизнес, и если их структура цен не принимается клиентом, то это его дело, решить, следует ли уменьшить цену соответственно или уйти от сделки (в этом случае, уйти от цен на алмазное сырье для того, чтобы, в конечном счете, спасти свою маржу). Разумеется, не имеет смысла получать убытки в конце года. Огранщики все еще считают себя привязанными к системе сайтхолдеров, несмотря на то, что доклад Рапапорт ясно показывает, что De Beers больше не является основным поставщиком сырья. Может быть, это потому, что они настолько привыкли к системе, боясь потерять престиж статуса сайтхолдера, или боятся потерять доступ к сырью. Независимо от психологических обоснований – устранение системы Sights и денег, которые они требуют, поможет огранщикам спасти свои операции.

Должны ли дилеры и трейдеры зависеть от Рапапорта?

Если Вы зайдете к любому дилеру бесцветных бриллиантов в любом офисе в алмазной бирже, то в самом центре рабочего стола Вы найдете знаменитый красный прайс-лист Рапапорта. Кажется, что их бизнес вращается вокруг этой красной бумаги, нравится ли им это или нет (у меня возникла визуальная ассоциация с китайским коммунистическим режимом, управляющим своими гражданами). Являются ли все дилеры всего лишь менеджерами собственного бизнеса, а Рапапорт истинным владельцем? Я вспоминаю жалобы дилеров в прошлом году, когда времена уже начинали быть непростыми, а Рапапорт продолжал понижать цены в прайс-листе. Люди теряли деньги, просто держа товарные запасы!

Знаменитый красный прайс-лист Рапапорта

Ни одна другая отрасль не имеет прайс-лист, управляемый одной организацией, как это происходит в алмазной промышленности. Где естественная свобода торговать по стоимости, на которую соглашаются обе стороны (это же устои капитализма)? Существует товар, есть покупатель, и есть продавец. Оба видят ценность товара. За сколько должен продавец продать? По какой цене следует покупателю купить его? Цена должна быть такой, чтобы оба чувствовали себя комфортно при покупке и продаже, зная, что каждый из них сможет получить прибыль при сделке. Первый курс – предмет Микроэкономика 101! Все просто – устранения прайс-листа Рапапорта, который управляет этой прибылью, избавит огранщиков от всех бед.

Возможно, что виноваты и розничные торговцы.

Что можно сказать о магазинах? Какова их роль в цепочке создания стоимости? Мы все знаем, что они получают наибольшие прибыли в этом цепочке. Может быть, они виноваты в снижении спроса со стороны потребителей? Если потребители могут тратить меньше денег сейчас, чем предыдущие годы, не должны ли розничные торговцы регулировать цены соответственно? Просто посмотрите на таблицу ниже, представляемую Bain & Co. и AWDC из года в год. Очевидно, что розничные торговцы получают крупнейшие прибыли. Да, мы знаем, что у них есть свои собственные расходы, которые требуется покрыть, а также многие другие компоненты вступают в игру, но все же, есть некоторые вина и на них. Как я уже говорил выше, снижение цены приведет к повышению спроса и росту спроса в дальнейшем по всем звеньям цепочки создания стоимости, совершенствования рынка для всех! (На самом деле это решение, которое принесет пользу большинству игроков на рынке).

Роль электронных торговцев в цепочке стоимости?

Однажды в не столь далеком прошлом, кто-то решил, что они откроют веб-сайт, и будут продавать бриллианты и ювелирные изделия через Интернет. Революция! Убрать фиксированную стоимость магазинов в торговых центрах, сократить расходы на персонал, оставаться открытым 24/7 и поделиться частью этой экономии с потребителями. Тем не менее, даже 20 лет спустя, на он-лайн продажи ювелирных изделий по-прежнему приходится гораздо меньше, чем 20% от всех продаж. Существует еще волшебный момент похода в магазин и физического ощущения мечты, любви. Тем не менее, тот факт, что потребители рассматривают помимо розничной торговли варианты, чтобы купить товар по более доступной цене, является наглядной демонстрацией того, что если бы ритейлеры снизили цены, они получили бы абсолютное увеличение совокупного спроса, и это решение повлекло бы за собой значительный сдвиг.

Революция

Первая революция в этой отрасли состоялось 1 марта 2015 года, когда большинство крупных индийских дилеров и огранщиков решили, что с них уже довольно “управления” Рапапортом их судьбой и решили положить конец этому! Что они сделали? Как я уже упоминал выше, они оценили все их запасы на RapNet по ценам прайс-листа Рапапорта. Это полностью исказило информация для Рапапорта и его банка данных информации, на которую он опирается. Посмотрите на различные таблицы индексов марта 2015 года на изображении выше. Посмотрите на текст таблиц (на самом деле, его отсутствие). В настоящее время он читается “Алмазный индекс RapNet (RAPI) это средняя цена для топ-25 параметров алмазов (D-H, IF-VS2). Он основан на 10 лучших ценах алмазов в каждой категории “. Это настоящий показатель? Является ли это истинным представлением отрасли? А как насчет других параметров цвета и чистоты? Разве они не играют важную роль в понимании истинного значения алмазов и состояние отрасли? Мы все знаем, что нынешнее основное требование менее развитых стран или стран, которые строят эту отрасль в настоящее время – это более низкое качество товаров по параметрам чистоты SI и цвета ниже, чем цвет H. Почему бы не ввести суб-индексы для того, чтобы всесторонне представлять рынок? Является ли RAPI в своем настоящем виде правильным представлением данных? Все эти вопросы сводятся к тому, что с учетом всего доверия, которое индустрия оказывает Рапапорту, может быть, она должна быть более скептически настроена. Принятие решений и скидки, основанные на неполных данных, возможно, были тенденцией в прошлом, но она не должна продолжаться. Может быть, после более тщательного рассмотрения дилеры осознают необходимость покончить с прайс-листом Рапапорта поскольку данные являются неполными и не приносят пользы. Продажи в соответствии с соглашениями между покупателями и продавцами позволили бы значительно улучшить прибыли для обеих сторон, так как рыночные силы, наконец, вступили бы в игру должным образом.

Текущий вид RAPI

Индустрия претерпевает фундаментальные структурные изменения

“Индустрия претерпевает фундаментальные структурные изменения” – это один немногих комментариев, сделанных Мартином Рапапортом в его докладе, с которым я согласен. Каждая отрасль проходит через неизбежные изменения и эволюцию, так как она движется вперед благодаря технологии или по любой другой причине. Алмазная промышленность, как и большинство отраслей, однажды напоминала пирамиду. На вершине были шахтеры, которые продавали сырье огранщикам, которые продают затем трейдерам и поставщикам, которые продают дистрибьюторам, а затем розничной торговле, и, наконец, потребителям, добавляя прибыль на каждом шагу, так же, как во многих других отраслях. Теперь, пирамида как стиль бизнеса трансформируется, и будет продолжать преобразования, пока не достигнет сбалансированной и гармоничной формы … круга. Что означает круг? Есть только 2 игрока: покупатель и продавец. Кто на самом деле диктует цены? Кто, в конце концов, обладает властью? Потребители и их деньги. Деньги правят всем.

Рассмотрим необработанный алмаз весом 1,111 карата, который был обнаружен Lucara Diamond Corporation, о чем было объявлено 19 ноября этого года. Генеральный директор компании заявил недавно, что он рассмотрит предложение $ 60 млн за этот камень. Это очень хорошая цена, но, если ни один покупатель не оценит этот камень на такую сумму, то, Вы, г-н генеральный директор, не получите желаемую цену. Я не утверждаю, что необработанный камень не стоит этих денег, поскольку я еще не видел его, и эта цена может быть очень привлекательной. Эксперт огранщик (один из многих) будет проверять и рассчитает оптимальный выход готовых бриллиантов, а затем скромный калькулятор возьмет на себя расчет стоимости алмаза. Мы видели много больших алмазов, которые хорошо продавались по цене свыше $ 54000 за карат, которые просит Lucara, но $ 60 млн по-прежнему большая сумма для любого покупателя. Тем не менее, Lucara получит именно столько, сколько их наилучший покупатель готов заплатить за алмаз, не более того. Это и есть воплощенная концепция власти в руках потребителя.

Необработанный алмаз весом 1,111 карат

Возвращаясь к сказанному ранее – E-магазины вступили в игру и выхватили кусок из бизнеса розничной торговли. Потребители желают приобрести алмазы за меньшие деньги, и они делают это таким же образом, как они сделали во многих других отраслях промышленности, убирая посредников и превращая пирамиды в круг. Разве не De Beers, и Аргайл делают это же самое, но обратным образом? Разве не De Beers, добывающая компания, основала De Beers Diamonds и открыла магазины, которые продают непосредственно потребителям (как я уже упоминал выше, Мартин Рапапорт спросил De Beers, имеют ли они намерения убрать дилеров совсем из цепочки … было ли Рапапорту известно, что De Beers уже имеет свои собственные торговые точки? Если это так, почему он спрашивал? Ответ будет очевиден. А если он не знал, то сейчас он знает!) Аргайл пришли к соглашению с ювелирной компанией Chow Tai Fook и начали производить ювелирной линии, убрав много поставщиков и оптовиков из цепочки создания стоимости. И в самом деле, а что в этом плохого? Производителям, конечно, нужно беспокоиться о собственном выживании. Эти две компании также определенно приняли концепцию круга!

Производители также должны отвечать перед своими акционерами в конце дня. Если De Beers снижает цену на 30-50%, к чему их призывает Рапапорт, то как будут реагировать акционеры? Что будет с ценой акций компании? Компании находятся под постоянным давлением со стороны акционеров с целью получения прибыли, в настоящее время это еще более актуально. Рапапорт не может ожидать, что De Beers примет на себя весь удар, тем более, что на рынке много других решений, которые смогут добиться аналогичных результатов для огранщиков!

Будущие прибыли

Я призываю Рапапорта сделать простое решение (и мудрое для себя) и по-настоящему стать защитником огранщиков, которым он пытается быть – прекратить публикацию прайс-листа! Да, это именно то, что я говорю. Сделает ли он это? Я бросаю вызов ему так же, как он это делает в отношении De Beers! Как вы думаете, что произойдет, если он это сделает? И я не имею в виду последствия для его организации Rapaport Group, которая нанимает много людей и имеет свои собственные расходы (возможно, он может просто продолжать торговать своими собственными бриллиантами?). Я имею в виду отрасль. Трейдеры и оптовики смогут выжить. Те, кто знает стоимость товара останется, остальные выйдут из бизнеса. Будет свободная торговля и огранщики начнут зарабатывать деньги снова. Звучит, как торжество рыночных сил.

Произойдут значительные слияния и поглощения, а также масштабные консолидации. Кое-кому, несомненно, придется уйти из цепочки. Производители, скорее всего, начнут скупать огранщиков, возможно, некоторые огранщики будет объединять силы с крупными дилерами, и, возможно, некоторые дилеры будут объединиться с предприятиями розничной торговли. Все это будет создавать стоимость путем сокращения расходов по всем направлениям, как и при любых других слияниях и поглощениях, о которых ежедневно объявляют в новостях. Новые компании и организации также будут возникать по мере того, как будет возвращаться прибыль и новые игроки захотят к этому приобщиться. Все это будет на благо потребителей, которые будут иметь больший выбор товаров, доступных по более низким ценам, чем раньше.

Может быть, компании по всей цепочке создания стоимости должны смотреть на королей бриллиантов, Лоуренса Граффа и Льва Леваева. Они являются вертикально интегрированными и обладают по сегменту на всем протяжении цепочки. Они владеют частично или полностью алмазными шахтами, они гранят алмазы, оправляют их в ювелирные изделия и продают их потребителям. Конечно, они оба имеют дело с самыми состоятельными потребителями, но, тем не менее, они должны быть примером того, как делается бизнес. Они оба чрезвычайно успешно и полностью игнорировали систему пирамиды.

Выводы:

Рапапорт должен взять на себя ответственность и признать, что его действия являются частично ответственным за состояние, в котором находится отрасль. Различным игрокам отрасли следует пересмотреть, как они управляют своим бизнесом. Все субъекты должны рассмотреть возможность консолидации их бизнеса с каким либо иным. Если отрасль в целом сделает шаг назад, отложит свое эго в сторону на секунду, начнет работать в команде, то отрасль двинется в целом вперед. Это будет беспроигрышный вариант для всех, особенно для потребителя, который уже сейчас теряет уверенность в отрасли и приобретает альтернативный продукт, что является верным смертным приговором для любой отрасли.

Я приглашаю всех встать в один ряд и работать совместно на общее благо. Запомните, бриллианты навсегда! Вопрос в том, кто останется навсегда с ними ….

Желаете что-то узнать или несогласны? Дайте мне знать в комментариях ниже!

Related Posts

- Graff Diamonds Always Offers First Class Pink Diamonds

- What Has Gone Wrong During The Sotheby’s Hong Kong Magnificent Jewels and Jadeite Auction?

- Christie’s New York Auction Sells Great Bulgari Vivid Blue Diamond

- Sotheby’s New York Misses Its Mark With Unsold Fancy Vivid Blue Diamond

- Christie’s Hong Kong Magnificent Jewels Sales Results Disappointing This Year

Leave a Reply

You must be logged in to post a comment.

Rapaport to be blamed for Industry Failure, not De Beers!

For over 35 years, the Rapaport Group has been publishing a weekly price list for colorless diamonds. What started as a hobby by its founder became the industry wide standard. You can find the first ever Rapaport list still hanging on the wall at the head office in Ramat Gan, Israel to remind us of the beginning of the end. Since those days, the Rapaport Group has also launched a diamond sales platform called Rapnet to allow for worldwide online diamond trading for industry participants, among the myriad of other services that they offer.

The turning point for the diamond industry market control was back in 2014 when the diamond market was faced with greater uncertainties. Martin Rapaport did what he did on any given week, reviewing and updating his price list according to his usual calculations. Only this time, it featured a huge drop in prices. It affected all those that feed him (via the membership fees that they pay to the Rapaport Group), causing many raised eyebrows at the sudden and significant change. There is also a significant conflict of interest that exists because Rapaport trades his own inventory despite the fact that he establishes prices on the Rap List. That can be a major cause for concern in his overall judgement in dropping the prices.

Over 1 million stones are listed for trade on Rapnet with over $8 billion in value, the online trading network for the industry’s buyers and sellers. When Rapaport revises this list in one way or another, the whole entire industry is greatly affected. This is because diamond dealers sell most goods (including on Rapnet) at a discount to the listed prices of the Rap List ,or on rare occasion at a premium price to the list. When the list is revised upwards, valuation of inventory goes up and when the price list is revised downwards, valuation moves accordingly. In short, the Rapaport List can take businesses up or down in one fell swoop. The Rapaport list directly affects the diamond prices of the diamonds on Rapnet (which you will recall is greater than 1 million in number and $8 billion in value).

Not everyone in the world was willing to sit back and let this continue. One morning during March 2015, the majority of dealers in the world, predominantly those that are located in India, decided to put the brakes on Rapaport and counter attack. They all listed their inventory on Rapnet at the Rapaport List prices (not below them). This in turn completely changed the game. No longer were the dealers allowing Rapaport’s judgement calls to dictate the game.

If you pay attention to diamond industry trends, you may have noticed that in the last few months, the Rapaport Index report has been a representation of “the average price for the top 25 diamond qualities (D-H, IF-VS2). it is based on the 10 best priced diamonds for each quality”. Is that even a proper representation of the industry? Can we trust this data? Why do we trust this data?

A view of the March 2015 RAPI Diamond Index prior to changes

A view of the March 2015 RAPI Diamond Index after the changes

A view of the March 2015 RAPI Diamond Index with commentaries

Why should De Beers fall to the pressure of Rapaport?

As a for profit organization, De Beers, like any other company out there in the world, has the right to charge or ask whatever price it wants for its products (as does any other diamond producer for that matter). In any industry, be it cars, food, clothing, or housing, the producer or manufacturer may ask his clients or any other potential client for any price for their goods. We are all capitalists in one way or another. If a polisher or manufacturer does not wish to accept the price that they are being quoted, they have the right to walk away from a deal. If enough manufacturers walk away, De Beers, and any other producer of rough diamonds, will realize that the prices are too high and will naturally reduce them to a level where the buyer will feel that they can buy product, transform it, and sell it for a profit. It is the basic economic law of supply and demand.

Martin Rapaport, in his monthly Rapaport newsletter, recently released an article blaming De Beers for artificially, prohibitively high rough diamond prices. As a supposed champion of the ‘everyman’ polishers and manufacturers, he elaborated over 6 pages how De Beers is essentially at fault for the current situation in the diamond industry. His claim is that the high prices for rough diamonds are causing all of the diamond trade to fall like dominoes as small- to medium- sized diamond manufacturers cannot meet the prices of the rough diamonds in order to buy, cut, polish and resell for a profit. He states that the profits are nonexistent because the diamond miners are greedily charging exorbitant prices for rough diamonds, forcing the polishers to borrow enormous loans from banks to pay for the goods. The banks were happily lending the money to the diamond industry and willing to only collect the interest payments for the loans because they had no problem with the money being funneled essentially directly to the mining companies, until the debt has now piled so high that even the banks are slowly pulling away from this scheme. Coupled with the fact that consumer demand for diamonds has remained relatively low due to the worldwide economic situation, it is as though the polishers and dealers are suffering from three fronts – De Beers’ prohibitively high prices, low consumer demand, and no more bank loans. By Martin Rapaport placing the blame squarely on De Beer’s shoulders, he is calling on them to take the hit and lower rough diamond prices ‘in order to save the industry in the long term’. This would allow the polishers a higher profit margin in the sales of their goods and allow them to recover.

Martin’s claim differs from the premise above in that he claims that the blame lies squarely in De Beer’s hands, while he does not acknowledge what was established above that if enough cutters, polishers, and manufacturers simply rejected the mining companies’ prices, that very factor would cause the price of rough diamonds to go down regardless (with De Beers and the other diamond mining companies taking the same hit). Martin calls on De Beers to do this and does not recognize the basic laws of economics that if only the same companies that rejected the RapNet tradition of listing below list price would use that same power and reject the prices of De Beers they could make another huge change for the second time in less than 2 years. Is there denial here about their power to affect change in the diamond industry? Rapaport makes a big claim in the article by saying that De Beers may have a master plan to eliminate the diamond trade entirely and eventually sell directly to the consumer, seemingly completely minimizing the diamond trade’s power and influence. He also entirely glossed over another 2 solutions to alleviate the situation – the retailers could charge less for the finished goods, causing consumer demand to rise and subsequently all demand to rise up the product manufacturing chain (higher demands for polished goods, higher demands for rough demands), which would translate into an improved situation for everyone – not just the polishers. Another solution is elaborated on below – stop putting out a price list and there will be no prices that the polished diamonds are held to, thus allowing for free market forces to determine the prices paid for goods and better profit margins to be earned.

So what came first? The chicken or the egg?

We all know that De Beers at one time was controlling not only the supply of diamonds but also their prices. We also know that since the late 1990’s De Beers lost that privilege, yet most polishers still believe it to be true. According to the Rapaport report, De Beers now controls about 46% of dollar sales but only 32.7% of volume, meaning that it no longer holds control. In fact, ALROSA produces more diamonds than De Beers does. According to Rapaport’s own report, De Beers does not have the power and control over the industry that the above mentioned Rapaport article is claiming that it has! This is interestingly contradictory. According to the table below, which is also part of the report that was written, there are 8 major companies controlling the market, and just 4% of the market is controlled by all the other smaller players. As you can see in the table, De Beers makes the largest amount of dollar sales but does not produce the most diamonds.

Mr. Rapaport, I have a question about this table: how come these 8 combined companies control 102%? Not to mention the last 4%, which totals 106%…. My calculator says that De Beers should be at 44%, Alrosa at 33%, and so on – according to the $ figures from your own table.

Diamond mining companies’ market shares

Polishers should make their own choices

For a short explanation of how buying from De Beers works – 90% of De Beers’ rough diamonds are sold by value to customers known as Sightholders, at events called Sights. This practice has existed now for a long time.

Polishers should have walked away from sights long ago. I think that polishers did not for a simple but innocent reason, believing that De Beers would simply replace them and they would just lose their supply. They did not believe that their walking away could have the effect that they desired. And if they had walked away from the sight system? If they were not making money anyway, why would they continue buying something at a dollar just to sell it at $0.90? What kind of business owner does that? Every business knows that they make money on 1 product, while losing on another, and yet at the end of the year they make money on their overall sales. However, it seems that polishers were losing money at the end of the year given both of those aspects of business. If I was a polisher, I would have shut down and moved on to another business!

Polishers were also falling to the pressure of traders not willing to buy the goods above a certain price, and therefore worked on very lean margins of no more than 2-3% (according to a Bain & Co. Report) because of the high prices of the rough diamonds and low prices of the polished diamonds. Every business owner makes his own decision on how to run his business, and if their price structure is not accepted by the client, it is up to him to decide to whether to reduce the price accordingly or to walk away from the deal (in this case, walking away from the rough diamond prices in order to ultimately save their margins). It certainly does not make sense to end the year at a loss. Polishers are viewing themselves as still beholden to the sightholder system despite the fact that the Rapaport report clearly shows that De Beers is no longer the main mine in town. Perhaps it is because they are so used to the system, afraid to lose the prestige of being a sightholder, or are afraid to lose what they think would be their only pipeline of goods. Regardless of the psychological justifications – eliminate the sights and the money that the polishers require to buy at sights, and the polishers would be rescuing their own operations.

Should Dealers & Traders Depend on Rapaport?

Walk into every dealer of colorless diamonds at any office of a diamond exchange and right in the middle of their desk you will find the famous red Rapaport price list. It seems that their business revolves around that red paper, whether they like it or not (which, by the way, just humorously gave me the mental visual association with the Chinese communist regime controlling their citizens). Are all the dealers just mere managers of their own businesses, and Rapaport the true owner? I recall listening to dealers’ troubles last year, when times were already starting to be tough, and yet Rapaport continued to reduce the price list. People were losing money just holding inventory!

The Rapaport famous red Price List Courtsey of rapaport

No other industry has a price list controlled by one entity like the diamond industry. Where is the natural freedom to trade at the value both parties agree on (the beating heart of capitalism)? There is a product, and there is a buyer and a seller. Both see value in the product. For how much should the seller sell it? At what price should the buyer buy it? At the exact price that both feel comfortable buying and selling, knowing each can make money in the transaction. Profit margins are therefore naturally determined. Microeconomics 101. Its that simple and eliminating the Rapport list that controls this margin would absolutely dig out the polishers from their woes.

Retail Shops May Also be at Fault

What about shops and stores? What is their role in the value chain? We all know that they account for the largest and fattest profits in this value chain. Maybe they are at fault for reduced demand by consumers? If consumers have less spending money now than previous years, shouldn’t the retailers adjust prices accordingly? Just look at the table below, presented year after year by Bain & Co. and the AWDC. It is clear that retailers account for the largest profits. Yes, we know that they have their own expenses to cover and many other components come into play, but still, there is some blame here for them to absorb. Like I stated above, lowered prices would lead to greater demand and subsequently greater demand along all of the steps of the value chain, improving the market for all! (This is actually the solution that benefits the most market players).

What Role Do E-Tailers Play in the Value Chain?

One day in the not so far past, somebody decided that they will open a website, and sell diamonds and jewelry over the internet. What a revolution! Cut the fixed cost of stores in malls, cut staff costs, stay open 24/7 and pass on some of those savings onto consumers. Yet even 20 years later, online jewelry sales still account for far less than 20% of all sales. There is still the magical moment of walking into a store and physically attaching oneself to the dream, to love. However, the fact that consumers are looking for outlets other than the retailers in order to buy product at a price that they are more willing to pay is a clear demonstration of the fact that if retailers lowered prices, they would absolutely increase aggregate demand and the solution above would be kick started into full gear.

Revolution

The first revolution in this industry took place on March 1, 2015, when the majority of large Indian dealers and polishers decided that they had enough with Rapaport “controlling” their destiny and decided to put an end to it! What did they do? As I mentioned above, they priced all their inventory on Rapnet at the Rapaport suggested price list’s list prices. This completely distorted information for Rapaport and his data bank of information on which he relies. Look at the various index tables from back in March 2015 in the image above. Look at the text below the tables (really, the lack thereof). Nowadays, it reads “the Rapnet Diamond Index (RAPI) is the average price for the top 25 diamond qualities (D-H, IF-VS2). It is based on the 10 best priced diamonds for each quality”. Is this a true index? Is this a true representation of the industry? What about the other colors and clarities? Do they not play an important role to understand true diamond value and the industry’s status? We all know that current major demand by less developed countries or countries who are building this industry currently demand lower quality goods in the SI clarities, and lower than H color. Why not have sub-indices in order to comprehensively represent the market? Is the RAPI as it currently stands a proper representation of data? All of these questions essentially raise the point that given all of the trust that the industry puts into Rapaport’s hands, maybe they should be more skeptical instead. Making decisions and deductions on incomplete data may have been the trend in the past but certainly does not need to continue. Maybe after taking a closer look, dealers will realize that they should ditch the incomplete Rap List altogether, with the obvious benefit that the data is incomplete and wasn’t properly contributing, but also that selling according to agreements between buyers and sellers would allow for significantly better profit margins for both parties as market forces would finally properly be at play.

The current representation of the RAPI

The Industry is Undergoing Fundamental Structural Change Anyway

“The industry is undergoing fundamental structural change” – this is 1 of probably only a handful of comments that Martin Rapaport made in his report with which I agree. Every industry goes through inevitable changes and evolution as it moves forward due to technology or any other reason to which it may be subjected. The diamond industry, like most industries, once resembled a pyramid. On top we had the miners, who sold to polishers, who sold to traders and suppliers, who sold to distributors, then on to retailers, and finally was sold to consumers, adding a desired profit margin at every step, exactly like many other industries. Now, the pyramid style business has transformed and will continue to transform until it will reach a balanced and harmonious form of…a circle. What is this circle? There are just 2 players; a buyer and a seller. Who really dictates prices? Who at the end of the day really has the power? Consumers and their money. Money is king.

Take the 1,111 carat rough white diamond that was discovered by Lucara Diamond Corporation, announced on November 19 of this year. The company’s CEO commented not long ago that he will entertain a $60 million offer on the rough. That is a very nice number, but, if no buyer values the rough at that price, well then Mr. CEO, you will not get your desired price. I am not suggesting that the rough is not worth that much as I have not yet seen it, and it just might be a bargain at this price. An expert polisher (one of many) will inspect and will calculate the best yield and then a humble calculator will take over and will decide the numerical value of the diamond. We have seen many large rough diamonds sell well above the $54,000 per carat that Lucara is looking for, but $60 million is still a large sum for any buyer to fork up. However, Lucara will only get as much as their top buyer is willing to pay for the diamond, and not more than that. This is entirely the concept of power in the hands of the consumer embodied.

The 1,111 carat rough diamond

Going back to my point – E-tailers came into the game and carved a piece out of the retailers’ business. Consumers desire to acquire diamonds for less money, and they are doing it in the same way that they have done in many other industries, by cutting out the most middle men possible from the value chain, turning that pyramid into a circle. Aren’t De Beers and Argyle doing just that, but reversed? De Beers the mining company started De Beers Diamonds and opened shops to sell directly to consumers (as I mentioned above, Martin Rapaport asked De Beers if they have the intentions of cutting dealers away out of the value chain…was Rapaport not aware that De Beers already has their own retail outlets? If so, why is he asking? The answer would be obvious. And if he did not know, now he does!) Argyle came to an agreement with jewelry company Chow Tai Fook and launched a jewelry line, cutting out many suppliers and wholesalers from the value chain. And really, what is wrong with that? Producers certainly need to worry about their own survival. These two companies are also definitely embracing the circle!

Producers also have to answer to their shareholders at the end of the day. If De Beers reduces their price by the 30-50% that Rapaport is calling for, then how will shareholders react? What will happen to the share price of Anglo-American? Companies are under constant pressure by shareholders for profits now more than ever. Rapaport can’t really expect that De beers will absorb all of the hit here, especially since so many other solutions exist in the market that will accomplish the same goal for the polishers!

Future Profits

I challenge Rapaport to do the easiest solution (effort-wise for himself) and to truly be the champion of the polishers that he is trying to be – stop publishing a price list! Yes that is exactly what I am saying. Will he? I am challenging him with the same manner as he is doing to De Beers! What do you think will happen if he does? And I am not referring to the ramifications to his organization the Rapaport Group that employs many people and has its own expenses to pay (maybe he can just continue trading his own inventory?). I am referring to the industry. Traders and wholesalers will still survive. Those that know the value of goods will remain, those that do not, will close up shop. There will be free trade, and polishers will start making money again. Sounds like economic force paradise.

There will be major M&A (mergers and acquisitions), as well as major consolidations. Some people in the value chain will undoubtedly have to go. Producers will most likely start buying up polishers, maybe some polishers will join forces with big dealers, and maybe some dealers will join forces with retailers. All of this will create value, by actually reducing costs across the board, just like any other major M&A announced daily in the news. New companies and entities will also arise as profits return to the table and new players will be thirsty to gain some for themselves, all to the benefit of consumers who will have a larger selection of goods available and at better prices than before.

Maybe companies from across the value chain should look at the king of diamonds, Mr. Lawrence Graff, and Mr. Lev Leviev. They are vertically integrated and carved themselves a piece of everything. They each own portions or even full diamond mines, they polish, and they set into jewelry and sell to consumers. Of course, they both deal with the highest ends of the affluent consumers, but nevertheless they should be the examples of how business is done. They are both extraordinarily successful and completely flout the pyramid system.

Conclusion

Rapaport should take responsibility and admit that his actions are partially responsible for the mess that this industry is in. Various players from the industry should reconsider how they manage and operate their businesses. All the entities should look into consolidating their businesses with complimentary ones. If the industry as a whole will take a step back, put their egos aside for a second, and work as a team, they will be able to push the industry as a whole forward. It will be a win-win for everybody, especially the consumer, who in the meantime is losing confidence in the industry, and walks to the next door shop and acquires an alternative product instead, a surefire death sentence to any industry.

I invite everybody to get on the bandwagon and work together for the sake of everybody. But remember one thing, diamonds are forever! The question is who will remain forever with them….

Wondering about anything or even disagree? Let me know in the comments below!

Related Posts

Leave a Reply

You must be logged in to post a comment.